Cycle Tested: Volume 1

Introduction:

I have spent the last 25 years professionally trading, investing, and building products. This has been across different organizations, asset classes and economic environments. I experienced the dot.com bubble, the subprime mortgage bubble, the creation and implosion of CDOs, the breaking of the buck, TARP, Brexit, and more than a couple of crypto winters.

Perhaps more importantly, I’ve spent a large portion of the last 25 years meeting and sharing ideas with some of the largest and most influential institutional investors in the world. Over the years I’ve been blessed to build relationships, and learn from these investors. Today, this remains the single most valuable, and enjoyable aspect of my role(s) at Hack VC and I would like to try and “pay it forward.”

Cycle Tested will share the most interesting discussion topics and recurring investor questions surrounding digital assets, FinTech, blockchain technology and AI.

- Peter Hans, Partner @ Hack VC

The Proliferation of Stable Coins.

I’ve spent a significant portion of the last quarter in meetings with institutional investors including current and prospective Hack VC LPs. While CryptoTwitter and media headlines gravitate towards near-term price action, the conversations with long-term investors are far different.

Most recently, conversations have centered around the convergence of traditional finance and blockchain rails, and most specifically surrounding the established product market fit and subsequent explosive growth of stable coins.

Below, I share two of the more common questions along with my thoughts:

1. "Why do we need so many stablecoins? Doesn't fragmentation hurt the mission of a global digital dollar?"

The reality is that "the dollar" isn't a monolith; it's a legal and functional wrapper. Given the rationales for different functional stables backed by the same assets, and the relative ease associated with launching one, we’re likely to continue moving away from the current duopoly. The major reasons behind this are:

- Jurisdictional Necessity: Under the GENIUS Act (2025), the U.S. has provided a federal framework for payment stablecoins. A key takeaway from that legislation is that it prohibits issuers from paying interest directly to holders. More recently, the OCC has chimed in that this also precludes staking rewards or other points-based compensation. That said, other nations will have different regulatory requirements where the design and features of the stablecoin may vary even if the underlying reference asset is the same.

- The "Sweep" Economy: This is where it gets interesting for firms like my former employer, Fidelity. To an end-user, $50,000 in a digital wallet is just "dollars." But if that user holds USDT, the yield on the underlying reserves goes to Tether. If that same user transfers the stablecoin to a centralized brokerage platform or exchange, Fidelity for example, that same third-party stablecoin could be swapped for FIDD. The individual investor sees no real difference, it’s just the entity capturing the NIM. This is functionally no different than an individual today transferring assets from one financial institution to another. For example, one could transfer funds from a Bank of America checking account to a Fidelity brokerage account and those dollars are then swept into a Fidelity cash account (a money market account). The major difference being that money market funds pay interest and stable coins do not.

- Apathetic Switching Costs: The real advantage comes in the assumption, which I think is probably correct, that not all entities will be in the NIM game and the switching costs aren’t worth it. In the above example, if the newly minted FIDD then is transferred externally via the customer’s Fidelity BillPay account to a merchant that has no horse in the race then does that recipient really care whether it’s Circle, Fidelity, Tether, or JPM who is pocketing the spread? In this environment, the advantages of funding costs are nomadic. This speaks to the power of owning the customer relationship and mindshare. It also speaks to why banks are so keen on the idea of tokenized deposits.

For legacy financial institutions, issuing a stablecoin is a defensive play to protect their MMF and sweep businesses, and an offensive play to capture zero cost AUM. Given these advantages and high margin profiles, we’re likely to see more competition and likely market bifurcation. It’s very possible that the existing players, USDT and USDC, dominate in payments and remittances for the foreseeable future while traditional brand name stables serve as more of the internal settlement and B2B asset.

2. Why hold a tokenized MMF vs a stablecoin?

The second question involves the role of Real-World Assets (RWAs), especially those tokenized securities such as Blackrock’s BUIDL and Fidelity’s FDIT, which could be functionally similar to a dollar-back stablecoin.

Interestingly, Fidelity has launched both a $1 NAV tokenized money market fund (FDIT) as well as a USD-backed stablecoin, FIDD. The logic here is that we will see a market bifurcation based on the intended use case. If one is paying for goods or services, analogous to how one would use a credit card today, the Fidelity client would use FIDD. However, should the customer be holding the asset, either in an account or as posted margin, then FDIT would be utilized in order to receive the benefit of interest income.

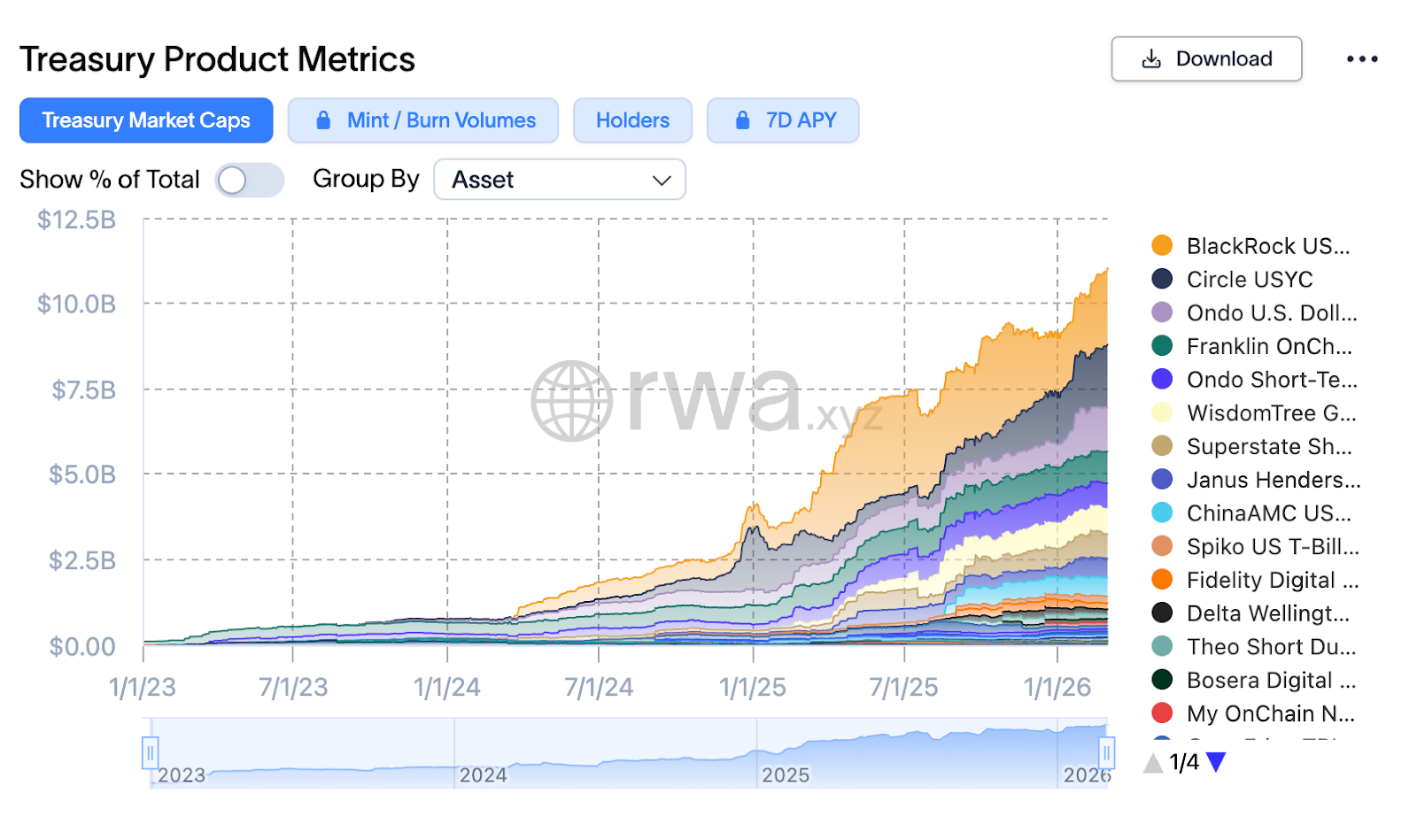

The tokenized Treasury market has been expanding rapidly over the past year and is currently north of $11B in AUM:

While the use case for stablecoins is clear and now widely accepted, the growth in tokenized treasury products also signifies a strong market use case.

In Summary:

We are at a key fulcrum of institutional adoption and are starting to see a turnover, or at least substantial expansion, of blockchain market participants and financial use cases. In the coming months and years, I believe that we will continue to see our global financial plumbing move to blockchain rails.

Disclaimer

This newsletter (the “Newsletter”) is being furnished on a confidential basis to a limited number of sophisticated investors (each a “Recipient”) on a “one‐on‐one” basis for the purpose of providing certain information about Hack VC Management, LLC and its affiliates, including the funds it manages (collectively, “Hack VC”). This Newsletter is for informational and discussion purposes only and is not, shall not be construed as, and does not constitute an offer, invitation, or recommendation by Hack VC to sell or a solicitation to subscribe for or buy any interest in or assets from Hack VC, nor shall any securities in or assets of Hack VC or any other entity be offered, issued or sold to, any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities or equivalent laws and regulations of such jurisdiction. Persons in possession of this Newsletter are required by Hack VC to inform themselves about any such restrictions and observe any such restrictions. Hack VC does not accept any liability to any person in relation to the distribution or possession of this Newsletter in or from any jurisdiction.

THIS NEWSLETTER IS FOR THE EXCLUSIVE USE OF THE PERSON TO WHOM IT IS ADDRESSED AND THEIR ADVISORS. IF THE RECIPIENT HAS NOT RECEIVED THIS NEWSLETTER FROM HACK VC, OR ANY ENTITY OR INDIVIDUAL AUTHORIZED BY HACK VC AS CONFIRMED BY HACK VC IN WRITING, OR YOU BELIEVE YOU RECEIVED THIS NEWSLETTER IN ERROR, PLEASE NOTIFY HACK VC IMMEDIATELY. THE UNINTENDED RECIPIENT MUST ALSO PERMANENTLY DELETE AND DESTROY ALL COPIES OF THIS NEWSLETTER FROM THEIR COMPUTER SYSTEM AND OTHER STORAGE DEVICES. UNINTENDED RECIPIENTS ARE HEREBY NOTIFIED THAT ANY DISSEMINATION, DISTRIBUTION, COPYING, OR US OF THIS NEWSLETTER AND THE INFORMATION CONTAINED HEREIN, IS STRICTLY PROHIBITED.

By accepting this Newsletter, the recipient agrees that it will, and will cause its representatives and advisors to, use the information only to inform itself about its investment in certain Hack VC funds or discuss its potential interest in Hack VC, as applicable, and for no other purpose and will not disclose any such information to any other person without the prior written consent of Hack VC. Any reproduction of this information in whole or in part is prohibited, and recipients agree to return this Newsletter to Hack VC upon request.

Past and targeted performance is not necessarily indicative of future results. There can be no assurance that Hack VC will achieve comparable results, that targeted returns, diversification or asset allocations will be met, or that Hack VC will be able to implement its investment strategy and investment approach or achieve its investment objectives for its investment vehicles. Statements contained in this Newsletter are based on current expectations, estimates, projections, opinions, and beliefs of Hack VC. Such statements involve known and unknown risks, uncertainties, and other factors, and undue reliance should not be placed thereon. Additionally, this Newsletter may contain “targets” or “forward‐looking statements”. Actual events or results or the actual performance of Hack VC may differ materially from those reflected or contemplated in such statements. As a result, investors should not rely on such forward‐looking statements, opinions, or beliefs in making investment decisions. No representation or warranty is made as to future performance or such forward-looking statements, options, or beliefs. Certain information contained herein (including forward‐looking statements, economic and market information, and portfolio company data) has been obtained from published sources and/or prepared by third parties (including portfolio companies) and, in certain cases, has not been updated through the date hereof. While such sources are believed to be reliable, neither Hack VC nor its respective affiliates or employees is making representations as to their accuracy or completeness, and they should not be relied on as such or be the basis for an investment decision. The information set forth herein does not purport to be complete and is subject to change, and Hack VC does not have any obligation to update such information or make any notification if such information becomes inaccurate.

Hack VC and its affiliates (including but not limited to its directors, officers, employees, and agents) do not accept any responsibility whatsoever or liability for any direct, indirect or consequential loss or damage suffered or incurred by any Recipient or any other person or entity however caused (including but not limited to negligence) in any way in connection with this Newsletter.

Hack VC is neither a law firm nor an accounting firm, and no portion of this document should be interpreted as legal, accounting, or tax advice. Hack VC is a registered investment adviser with the United States Securities and Exchange Commission (the “SEC”). Registration of an investment adviser with the SEC does not imply any level of skill or training.